Open Banking vs. Firm Banking: What's the Difference?

Why Bank Pay runs on open banking — and how open banking and firm banking differ structurally.

Bank Pay is built on open banking

Bank Pay runs on an open banking infrastructure.

When money moves between accounts, the underlying rail is either firm banking or open banking. What's the difference?

Before answering that, it helps to first distinguish between a transfer and a remittance.

Transfer vs. remittance

Both involve moving money, but they differ in how.

A transfer is a direct movement of funds from a customer's bank account to a merchant's bank account — the conventional, straightforward path.

A remittance involves a prepaid wallet in the flow. For example, when a Kakao Pay user doesn't have a balance, they send money from their registered account to Kakao Pay first — that's a remittance.

All transactions between financial institutions flow through the Electronic Financial Network.

Depending on who connects to that network, the rail is classified as either firm banking or open banking.

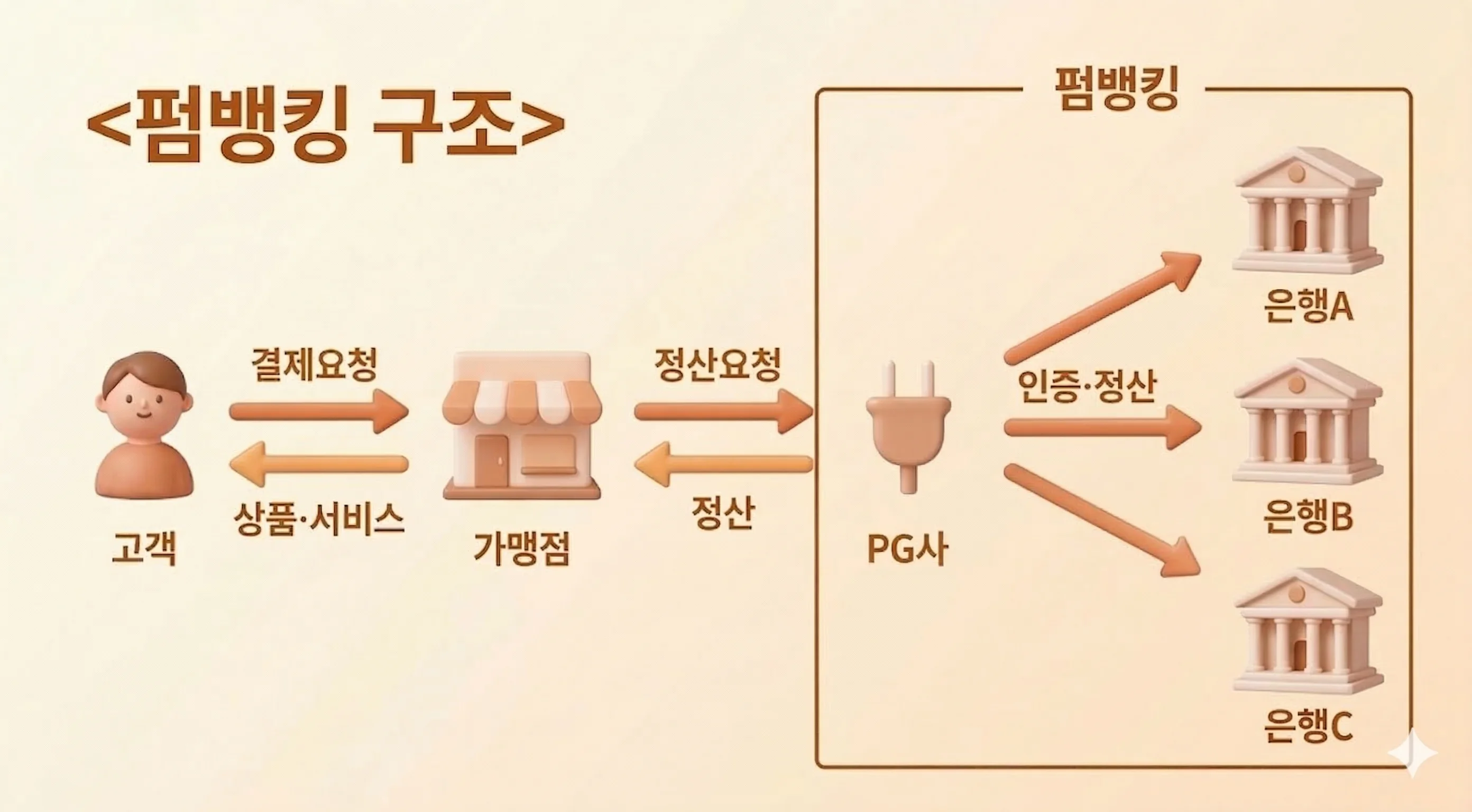

What is firm banking?

Firm banking is the legacy platform of the Electronic Financial Network.

In this model, a payment processor connects directly to each bank to handle transactions. It's designed to deliver complete financial services within a single institution, with a strong emphasis on reliability.

Firm banking is enterprise-oriented — built for high-volume fund transfers and corporate treasury management.

What is open banking?

In open banking, the connection between institutions runs through the Korea Financial Telecommunications and Clearings Institute (KFTC) rather than directly between a payment processor and a bank.

Open banking was created to reduce bank fees and promote fintech growth. Transaction fees are roughly 1/10th the cost of traditional firm banking rates.

Data is exchanged through standardized APIs, and the model is designed to create an open ecosystem where multiple providers can serve customers on a level playing field.

Why Bank Pay uses open banking

Open banking ties fees to the service a consumer selects, which means the system is fundamentally designed to give users more choice rather than locking them into a single institution.

That consumer-oriented design — flexibility, variety, and competitive pricing — fits Bank Pay's goals well. Firm banking, by contrast, prioritizes stability and structured processes for enterprise use cases.

Because Bank Pay is built for individual consumers with diverse transaction patterns, open banking is the right infrastructure.

| Firm banking | Open banking | |

|---|---|---|

| Connected through | Payment processor ↔ bank (direct) | KFTC (intermediary) |

| Target audience | Enterprise | Fintech and consumer services |

| Emphasis | Stability and consistency | Variety and user choice |

| Fee level | Relatively high | ~1/10th of traditional rates |

Bank Pay uses open banking to deliver consumer-tailored service at a lower fee structure.

Need technical support?

Code Samples

HectoFinancial GitHub